Mpower vs Prodigy Finance: Which No-Cosigner Loan is Best?

Introduction: The New Era of No-Cosigner Loans

For international students, 2026 is a year of both opportunity and high costs. As tuition fees in the USA and Canada continue to rise, the traditional banking system in India—which often demands property collateral—is becoming a bottleneck. This guide explores the two most powerful alternatives: Mpower Financing and Prodigy Finance. We will analyze why these “Fintech” lenders are the only hope for students without a US-based cosigner.

Chapter 1: The Eligibility Crisis – Can You Get Approved?

Before looking at interest rates, you must know if you qualify. Both lenders use proprietary algorithms, but their focus differs.

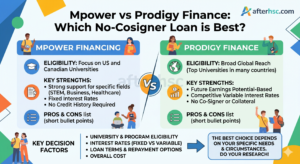

Mpower Financing Eligibility (2026 Update)

-

Academic Range: Mpower supports both Undergraduate (last 2 years) and Graduate students.

-

University List: They support ~400 schools in the US and Canada.

-

Country Support: They fund students from 190+ countries, including India, Nigeria, and Brazil.

-

Credit History: You do not need a US credit history. However, they will check your local credit score (like CIBIL in India).

Prodigy Finance Eligibility (2026 Update)

-

Academic Range: Prodigy focuses almost exclusively on Postgraduate (Masters and MBA) programs.

-

Course Specialization: They prefer STEM, Business, Public Policy, and Law.

-

University List: Prodigy has a much larger reach with over 850+ schools globally, including the UK, Europe, and Australia.

-

Pre-Approval: You can get a “provisional offer” even before you have your final admission letter.

Chapter 2: The Visa Process – Turning a Loan into an I-20

A loan is useless if it doesn’t get you a visa. This is where Mpower and Prodigy differ the most.

Mpower’s Visa Support Advantage

Mpower is famous for its “Visa Support Letter.” Once conditionally approved, they provide a document that US and Canadian embassies recognize as “Proof of Funds.”

-

Speed: Usually issued within 3–5 days.

-

Success Rate: Very high, as the letter clearly states the funds are non-collateralized and dedicated to the student.

Prodigy’s Sanction Process

Prodigy requires a USD 500 processing fee before they issue the final sanction letter. While this is an upfront cost, the letter is extremely robust for visa interviews in the UK and Europe.

Chapter 3: Deep Dive into Repayment – Managing Your Debt

Mpower’s Simple Interest Model

During your studies and the 6-month grace period, Mpower requires you to make interest-only payments.

-

The Benefit: You build a US credit score while you are still in school. By the time you graduate, you might already have a 700+ FICO score, making it easier to rent an apartment or get a credit card.

Prodigy’s Full Moratorium Option

Prodigy offers a Full Moratorium. This means you pay zero dollars while studying.

-

The Risk: Interest “capitalizes.” This means the interest is added to your principal amount. While you save money today, your total loan amount grows significantly by the time you graduate.

Chapter 4: Hidden Fees and “The Fine Print”

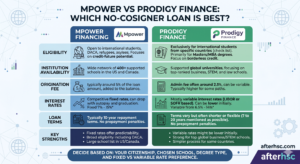

| Fee Type | Mpower Financing | Prodigy Finance |

| Origination Fee | ~5% (Added to total loan) | ~2.5% to 5% (Admin fee) |

| Early Repayment | $0 Penalty | $0 Penalty |

| Upfront Cost | $0 | $500 (Sanction fee) |

| Autopay Discount | 0.25% Reduction | No Standard Discount |

Chapter 5: Which One is Cheaper in 2026?

If the US Federal Reserve increases interest rates in 2026, Mpower becomes the winner because your rate is Fixed. If the market remains stable or rates drop, Prodigy’s Variable Rate could potentially save you thousands of dollars in the long run.

Chapter 6: Step-by-Step Guide to Applying for a No-Cosigner Loan

Applying for an international student loan is a multi-stage process. Both Mpower and Prodigy have streamlined digital applications, but the documentation phase is where most students get stuck.

Phase 1: Pre-Application Research

Before you hit “Apply,” you must check the School Support List.

-

Action: Visit the lender’s website and use the “Check Eligibility” tool. Enter your school name and your specific degree.

-

Pro Tip: If your school is not listed, you cannot apply. Prodigy supports more schools (850+), while Mpower is more selective (~400).

Phase 2: The Initial Application (15 Minutes)

This is the easiest part. You will provide:

-

Personal details (Name, Address, Citizenship).

-

Academic plans (School name, Program, Expected graduation date).

-

Funding amount requested (Tuition + Living expenses).

Phase 3: The Conditional Offer

If you pass the initial screening, you receive a Conditional Offer. This document outlines your estimated interest rate and maximum loan amount.

-

Note: This is not a final contract. It is a “look at what we can offer you” stage.

Phase 4: Document Upload & Verification (The Critical Stage)

You will need to provide high-quality scans of:

-

Valid Passport: Ensure it has at least 6 months of validity.

-

University Admission Letter: Must be for the term you are applying for.

-

Past Academic Transcripts: Marksheets from your previous degree (e.g., Bachelor’s).

-

English Proficiency Test Scores: IELTS, TOEFL, or Duolingo.

-

Resume/CV: Detailing your work experience (crucial for Prodigy).

-

Financial Proof: Any savings or other scholarships you are using.

Phase 5: The Final Sanction & Visa Support

Once documents are verified, the lender performs a final review.

-

Mpower: Issues a Visa Support Letter for free.

-

Prodigy: Requires a matching fee/processing fee (approx. $500) before issuing the final letter.

Chapter 6: Step-by-Step Guide to Applying for a No-Cosigner Loan

Applying for an international student loan is a multi-stage process. Both Mpower and Prodigy have streamlined digital applications, but the documentation phase is where most students get stuck.

Phase 1: Pre-Application Research

Before you hit “Apply,” you must check the School Support List.

-

Action: Visit the lender’s website and use the “Check Eligibility” tool. Enter your school name and your specific degree.

-

Pro Tip: If your school is not listed, you cannot apply. Prodigy supports more schools (850+), while Mpower is more selective (~400).

Phase 2: The Initial Application (15 Minutes)

This is the easiest part. You will provide:

-

Personal details (Name, Address, Citizenship).

-

Academic plans (School name, Program, Expected graduation date).

-

Funding amount requested (Tuition + Living expenses).

Phase 3: The Conditional Offer

If you pass the initial screening, you receive a Conditional Offer. This document outlines your estimated interest rate and maximum loan amount.

-

Note: This is not a final contract. It is a “look at what we can offer you” stage.

Phase 4: Document Upload & Verification (The Critical Stage)

You will need to provide high-quality scans of:

-

Valid Passport: Ensure it has at least 6 months of validity.

-

University Admission Letter: Must be for the term you are applying for.

-

Past Academic Transcripts: Marksheets from your previous degree (e.g., Bachelor’s).

-

English Proficiency Test Scores: IELTS, TOEFL, or Duolingo.

-

Resume/CV: Detailing your work experience (crucial for Prodigy).

-

Financial Proof: Any savings or other scholarships you are using.

Phase 5: The Final Sanction & Visa Support

Once documents are verified, the lender performs a final review.

-

Mpower: Issues a Visa Support Letter for free.

-

Prodigy: Requires a matching fee/processing fee (approx. $500) before issuing the final letter

Chapter 6: Step-by-Step Guide to Applying for a No-Cosigner Loan

Applying for an international student loan is a multi-stage process. Both Mpower and Prodigy have streamlined digital applications, but the documentation phase is where most students get stuck.

Phase 1: Pre-Application Research

Before you hit “Apply,” you must check the School Support List.

-

Action: Visit the lender’s website and use the “Check Eligibility” tool. Enter your school name and your specific degree.

-

Pro Tip: If your school is not listed, you cannot apply. Prodigy supports more schools (850+), while Mpower is more selective (~400).

Phase 2: The Initial Application (15 Minutes)

This is the easiest part. You will provide:

-

Personal details (Name, Address, Citizenship).

-

Academic plans (School name, Program, Expected graduation date).

-

Funding amount requested (Tuition + Living expenses).

Phase 3: The Conditional Offer

If you pass the initial screening, you receive a Conditional Offer. This document outlines your estimated interest rate and maximum loan amount.

-

Note: This is not a final contract. It is a “look at what we can offer you” stage.

Phase 4: Document Upload & Verification (The Critical Stage)

You will need to provide high-quality scans of:

-

Valid Passport: Ensure it has at least 6 months of validity.

-

University Admission Letter: Must be for the term you are applying for.

-

Past Academic Transcripts: Marksheets from your previous degree (e.g., Bachelor’s).

-

English Proficiency Test Scores: IELTS, TOEFL, or Duolingo.

-

Resume/CV: Detailing your work experience (crucial for Prodigy).

-

Financial Proof: Any savings or other scholarships you are using.

Phase 5: The Final Sanction & Visa Support

Once documents are verified, the lender performs a final review.

-

Mpower: Issues a Visa Support Letter for free.

-

Prodigy: Requires a matching fee/processing fee (approx. $500) before issuing the final letter.

-

Mpower vs Prodigy Finance Which No-Cosigner Loan is Best

Chapter 7: Comparing International Fintech Loans vs. Indian Nationalized Banks

Many students wonder: “Why take a USD loan at 12% when an Indian bank offers 10% in INR?” This section explains the financial logic.

1. The Collateral Factor

Indian banks (SBI, BoB) almost always require a property or an FD as security. If you don’t have a bungalow or land to pledge, your application is dead. Mpower and Prodigy remove this barrier.

2. Currency Depreciation

The Indian Rupee (INR) historically depreciates against the US Dollar (USD) by about 3-5% every year.

-

If you take an INR loan, your debt stays in INR, but you earn in USD.

-

Taking a USD loan means you borrow in the same currency you will earn in, protecting you from exchange rate fluctuations during repayment.

3. Ease of Disbursement

Indian banks often require a lot of paperwork every semester to release funds. Mpower and Prodigy pay the university directly and automatically. This reduces your stress during exam seasons.

Chapter 8: Repayment Strategies for 2026 and Beyond

Strategy A: The “Aggressive Principal” Method

Since neither lender has a prepayment penalty, you should pay more than your EMI as soon as you start your OPT or H1-B job. Every extra $100 you pay goes directly toward the Principal, significantly reducing your interest over 10 years.

Strategy B: Refinancing Post-Graduation

Once you have been working in the USA for 6–12 months and have a high US Credit Score, you can Refinance your loan with US-based lenders like SoFi or Earnest. This can drop your interest rate from 12% down to 5-7%.

Chapter 9: Frequently Asked Questions (The Ultimate Student Finance FAQ)

Q1: Do I really not need a cosigner for Mpower or Prodigy?

Answer: Yes. Both lenders are designed for students who do not have a US-based cosigner or family members with property to pledge as collateral. They use your “Future Earning Potential” based on your university and major to approve the loan.

Q2: Which lender is better for MBA students?

Answer: Prodigy Finance generally has a stronger relationship with top-tier global business schools. However, Mpower is excellent for specialized MBA programs in the US and Canada. You should apply to both to see who offers the lower rate.

Q3: Can I get a loan for living expenses, or only tuition?

Answer: Prodigy Finance can often cover 100% of the cost of attendance, including rent and food. Mpower has a lifetime limit of $100,000; if your tuition is $60,000, you can use the remaining $40,000 for living expenses.

Q4: What happens if I can’t find a job after graduation?

Answer: Both lenders offer “Forbearance” or “Deferment” options during financial hardship. Mpower also offers the Path2Success program to help you with career coaching to ensure you land a high-paying job.

Q5: Does Mpower or Prodigy check my Indian CIBIL score?

Answer: Yes. While they don’t require US credit history, they will perform a “Soft Credit Check” on your home country’s credit bureau to ensure you don’t have existing defaults.

Q6: Are the interest rates fixed or variable?

Answer: Mpower offers Fixed Rates (they never change). Prodigy offers Variable Rates (they fluctuate based on market benchmarks like SOFR).

Q7: How is the money sent to the university?

Answer: The funds are disbursed directly to the university’s financial aid office. You don’t have to worry about handling the transfer or currency exchange yourself.

Q8: Can I pay off the loan early?

Answer: Absolutely. Neither lender charges a “Prepayment Penalty.” Paying off your loan early is the best way to save thousands of dollars in interest.

Q9: Do they support Undergraduate degrees?

Answer: Mpower supports students in their final two years of Undergraduate study. Prodigy focuses primarily on Graduate (Masters/MBA) programs.

Q10: Is a 12% USD loan better than a 10% INR loan?

Answer: Often, yes. Because you will be earning in USD, a USD loan protects you from the depreciation of the Rupee. If the Rupee falls 5% against the Dollar, your INR loan effectively becomes more expensive to pay back with your USD salary.

Q11: What is an “Origination Fee”?

Answer: It is a one-time administrative fee charged by the lender for processing the loan. It is usually added to your total loan balance rather than being paid out of pocket.

Q12: How long does the approval process take?

Answer: If your documents are in order, you can get a conditional offer in 24 hours. The full verification and sanction process usually takes 2 to 4 weeks.

Q13: Can I use the loan letter for my F-1 Visa interview?

Answer: Yes. The “Visa Support Letter” provided by Mpower and the “Sanction Letter” from Prodigy are both accepted by US and Canadian consulates.

Q14: Do they fund PhD students?

Answer: Support for PhDs is limited and depends on the specific university and research funding. STEM PhDs have a higher chance of approval.

Q15: What is the grace period?

Answer: Both lenders offer a “Grace Period” (usually 6 months) after graduation where you only pay interest (or zero in some cases) while you look for a job.

Q16: Are there any discounts available?

Answer: Mpower offers a 0.25% discount if you set up Autopay from a US bank account.

Q17: What if my university is not on their list?

Answer: If your school isn’t supported, you cannot get a loan from them. You should check both lists as they update them frequently.

Q18: Can I refinance these loans later?

Answer: Yes. Once you have a job in the US and a good credit score, you can refinance with companies like SoFi to get a much lower interest rate.

Q19: Is health insurance included in the loan?

Answer: If health insurance is part of the “Cost of Attendance” listed by the university, the loan can cover it.

Q20: Why should I trust [suspicious link removed] for this info?

Answer: At AfterHSC, we provide the most updated 2026 data based on direct lender policies to ensure international students make informed financial decisions.